Markets follow a pattern that is as persistent as it is costly: the most enthusiastic buyers tend to arrive near the end of the cycle. We’ve seen it repeatedly in diverse speculative manias—technology stocks in 2000, financials and housing in 2006, cryptocurrencies in 2021. The sequence rarely changes. Prices of the asset(s) begin rising quietly, early buyers benefit, and gradually attention builds. Media coverage expands, success stories circulate, and what started as an opportunity becomes a widely discussed phenomenon.

At that point, participation shifts from early informed buyers to the retail public. What was once driven by analysis becomes driven by observation—who is making money, what is trending, what others are saying. The market stops being a place of independent judgment and becomes a social feedback loop.

Understanding why investors buy market peaks requires stepping outside traditional finance theory. Markets are not just information-processing machines as proposed by the efficient market theorists Eugene Fama et al; they are environments where human psychology, decision-making uncertainty, money and social influence intersect.

In theory, investors are rational. In practice, they are influenced—often heavily—by what others believe and do. As prices rise, narratives emerge:

- “This time is different.”

- “Everyone is making money.”

- “The opportunity is obvious.”

These narratives gain credibility not because they are rigorously validated, but because they are widely repeated. This is social proof at work. When enough people believe something, it begins to feel true. Over time, investors stop asking, “What is this worth?” and start asking, “Why isn’t everyone already in this?” That shift sets the stage for both FOMO and herding to take over.

FOMO: The Emotional Trigger

Fear of Missing Out is often the ignition point that pulls investors into overheated assets.

Importantly, FOMO is not just about greed—it is rooted in something deeper:

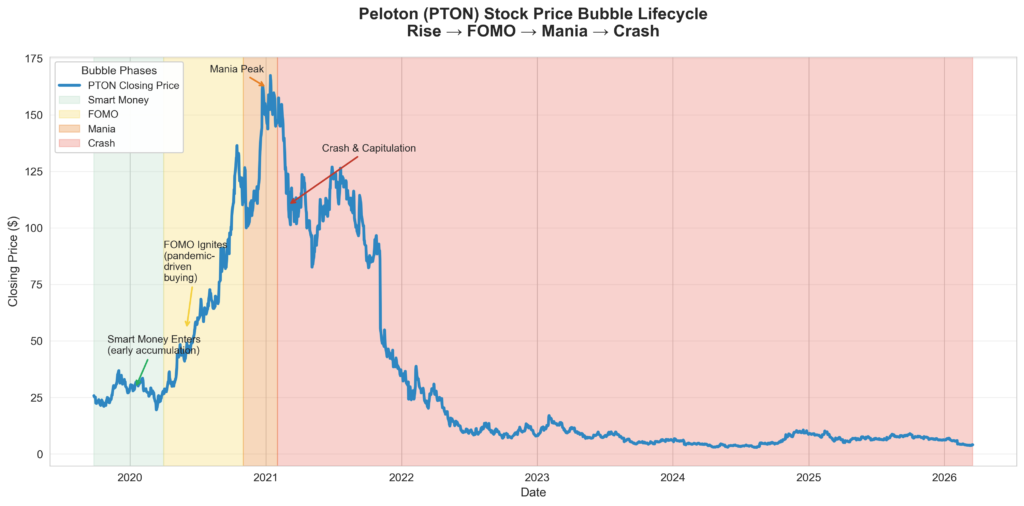

a fundamental human instinct to avoid social exclusion. Humans evolved to survive in groups. Being excluded from the group historically carried severe consequences possibly even death. Modern markets exploit that instinct. When investors see friends, coworkers, or social media personalities making money in a particular asset, the emotional response is immediate.The chart below shows the Peloton stock which became very popular during the pandemic, color codes correspond to different phases smart money buying early vs FOMO drven buyers vs the Mania peak with the stock price over $150 and the last phase the crash.

In markets, this plays out in subtle but powerful ways. Investors observe others succeeding—friends discussing gains, headlines highlighting windfalls, social media amplifying winners. The signal is consistent and hard to ignore:

Other people are benefiting from something you are not part of. That perception creates internal pressure:

- “Why am I not participating?”

- “Am I overlooking something obvious?”

- “Am I the only one missing this?”

At this point, the decision framework begins to change. The core question is no longer: “Is this a good investment at this price?” The question becomes: “Can I afford to stay out?” This is a critical inflection point. The investor is no longer evaluating value—they are reacting to perceived opportunity loss relative to others and social exclusion.

Social proof reinforces the effect. The more visible the success of others becomes, the more credible—and urgent—the opportunity appears. Even skeptical investors can be pulled in as the number of participants grows.

FOMO doesn’t eliminate rational thinking entirely. It simply reorders priorities, placing social validation ahead of independent objective analysis. That is often where discipline begins to erode.

Herding Behavior: The Crowd Effect

If FOMO is the trigger, herding is the mechanism that drives markets to extremes.

Herd behavior occurs when individuals align their actions with the group, implicitly assuming the group possesses superior insight. In uncertain environments—like financial markets—this tendency becomes even stronger.

The logic is simple, even if flawed: If so many people are buying, they must know something.

This belief is reinforced by visibility. Rising prices validate prior buyers, attract new participants, and create a self-reinforcing cycle. Institutions observe peers outperforming and adjust accordingly. Retail investors follow what is trending. Strategies converge.

Independent thinking quietly gives way to collective behavior.

In practical terms, herding shows up as:

- Capital flowing into the same “must-own” assets

- Portfolios becoming increasingly similar

- Popular trades becoming crowded trades

The irony is that this collective confidence tends to peak when risk is highest. By the time an asset achieves broad consensus:

- valuations are elevated

- expectations are stretched

- future returns are constrained

The crowd, by definition, is late—not because individuals lack intelligence, but because social confirmation arrives after prices have already moved. In the end, herding doesn’t just explain why investors buy rising assets.It explains why they often do so at precisely the wrong time.

Recency Bias: Why Rising Markets Feel Safe

Another behavioral force contributing to market peaks is recency bias. Recency bias causes investors to overweight recent events when predicting the future. If a particular set of assets have risen for several years, the human brain begins to assume that rising prices are the normal state of the world. The mental model becomes: “Prices have been going up — therefore they will continue going up.” Risk begins to feel invisible. But market history shows that the illusion of safety is greatest just before the largest, most painful corrections.

How Speculative Bubbles Form

These psychological forces combine into a predictable cycle.

- Early opportunity emerges – informed buyers

- Prices begin rising – the breakout

- Media attention increases

- Narratives develop

- FOMO spreads

- The crowd rushes in

- Prices go parabolic

- Reality eventually intervenes – the reversal

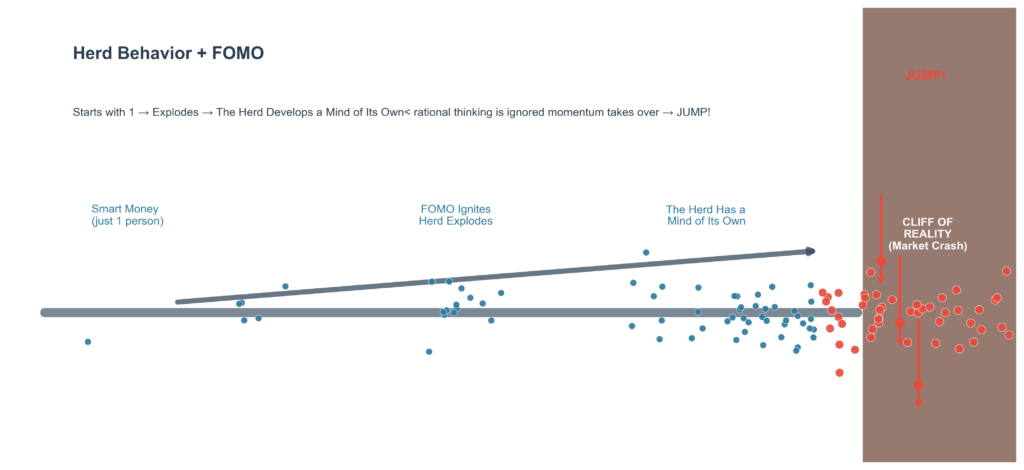

The final stage is where the majority of new buyers appear. Paradoxically, the moment when investors feel the most confident often corresponds to the point where future returns are lowest. The chart Herd Behavior + FOMO visualizes the large number buyers entering the stock just before the stock falls off a cliff

Why Intelligent Investors Still Fall Into the Trap

This isn’t about intelligence. Even experienced, disciplined investors get pulled into crowded trades at the wrong time. The reason is simple: markets are social environments, not just analytical ones.

When outcomes are uncertain—and they always are—people naturally look outward for cues. What are others buying? What’s working right now? What’s everyone talking about?

Over time, repetition turns narrative into perceived truth. A story heard often enough begins to feel like truth. That’s how rational analysis quietly gives way to social confirmation—and why even thoughtful investors can end up buying at the peak.

The Practical Solution: Minimize the Influence of Hype

You don’t need to eliminate emotion—that’s unrealistic. What works is building a robust investment process that reduces how much emotion can influence decisions at critical moments. The most effective investors tend to rely on a few simple anchors:

- objective security selection frameworks

- predefined decision rules

- diversification across strategies and time

- patience when opportunities are scarce

The goal isn’t to perfectly time markets. It’s to avoid being pulled in by hype when prices already reflect overly bullish growth expectations.

Actionable Takeaways for Investors

1. Separate narrative from data

When an investment becomes popular, pause and ask: What is the actual evidence?

Narratives spread quickly because they are easy to understand and repeat. Data—cash flows, margins, valuation—moves much slower and is harder to distort.

A useful discipline is to write down the key assumptions required to justify the current price. If those assumptions feel stretched, they probably are.

Supporting research: Barberis, Shleifer, and Vishny (1998) show how investors overreact to narratives and recent information, leading to mispricing.¹

2. Be skeptical of parabolic price moves

Sharp, accelerating price increases often signal that expectations—not fundamentals—are driving returns.

By the time an asset “goes vertical,” a great deal of optimism is already embedded in the price. Historically, these environments have produced asymmetric risk, where upside potential becomes limited and downside risk expands. Parabolic moves don’t reduce risk—they often magnify the risk.

Supporting research: De Bondt and Thaler (1985) document how extreme price moves tend to reverse over time, consistent with investor overreaction.²

3. Develop a rules-based investment process

A simple, predefined process can act as a buffer between emotion and action. This might include:

- valuation thresholds for entry

- position sizing rules

- systematic rebalancing

The key benefit is consistency. When decisions are guided by rules rather than impulse, investors are less likely to chase what’s working in the moment. Well-designed investment processes don’t eliminate mistakes—but they help mitigate big, avoidable risks.

Supporting research: Asness, Moskowitz, and Pedersen (2013) highlight the long-term robustness of systematic value and momentum strategies across markets.³

4. Pay attention to sentiment indicators

Indicators that quantify sentiment and measurements of extreme optimism are often more informative than fundamentals at market peaks.

Signals to watch:

- surging trading volume

- spikes in speculative options activity

- saturation media coverage and “can’t lose” narratives

When an idea becomes universally accepted, the market has usually already priced in that consensus. Sentiment doesn’t tell you exactly when a reversal will happen—but it can tell you when risk is no longer being respected.

Supporting research: Baker and Wurgler (2006) show that high investor sentiment is associated with lower subsequent returns, particularly for speculative assets.⁴

5. Remember that patience is a competitive advantage

In a world of constant information and pressure to act, patience is rare—and valuable.

Many of the strongest long-term returns come from waiting for dislocations, not chasing momentum. Mean reversion and value-oriented approaches rely on this principle: buying when expectations are low, not when they are elevated.

Patience doesn’t feel productive in the moment. But over time, it is often what separates disciplined investors from reactive ones.

Supporting research: Fama and French (1992) document the long-term return premium associated with valuation-based investing, consistent with mean reversion effects.⁵

Final Thoughts

Markets will always contain elements of psychology, storytelling, and social influence. FOMO, herd behavior, and recency bias are not temporary anomalies — they are permanent features of human behavior. Understanding these factors does not eliminate risk. But it can help investors recognize when emotions are beginning to drive their decisions. And in markets, the simple ability to avoid the crowd when the emperor is discovered to have no clothes can be more valuable than predicting the next big winner.

References

- Barberis, N., Shleifer, A., & Vishny, R. (1998). A Model of Investor Sentiment. Journal of Financial Economics.

- De Bondt, W., & Thaler, R. (1985). Does the Stock Market Overreact? Journal of Finance.

- Asness, C., Moskowitz, T., & Pedersen, L. (2013). Value and Momentum Everywhere. Journal of Finance.

- Baker, M., & Wurgler, J. (2006). Investor Sentiment and the Cross-Section of Stock Returns. Journal of Finance.

- Fama, E., & French, K. (1992). The Cross-Section of Expected Stock Returns. Journal of Finance.