Agustin Leon, CFA | Founder of Behavioral CIO

You’re intelligent. You read the reports. You follow the news. You’ve done everything “right” — yet somehow, your portfolio keeps underperforming. The market climbs, and you’re still behind. You make a move with conviction, and it costs you. You freeze when you should act, and act when you should do nothing.

What if the problem isn’t the market at all?

What if the biggest risk in your portfolio isn’t geopolitical instability, rising interest rates, or an earnings miss — but the three pounds of brain matter sitting between your ears?

Welcome to behavioral finance: the discipline that sits at the intersection of psychology and economics, and has spent decades proving that human beings are not the rational actors classical theory assumed us to be. Introduced to mainstream thought by Nobel Prize-winning psychologist Daniel Kahneman and his collaborator Amos Tversky, behavioral finance reveals that our minds are riddled with systematic cognitive shortcuts — heuristics — that served our ancestors well on the savanna hunting wild game but are quietly devastating in the modern capital markets.

There’s a term for what these biases cost you: the behavioral gap. Research from DALBAR’s Quantitative Analysis of Investor Behavior has consistently shown that while the S&P 500 has historically delivered returns in the range of 10% annually before inflation, the average equity investor has captured only a fraction of that — often as little as 3–4% — not because of bad markets, but because of bad timing driven by emotional decision-making. That gap is not bad luck. That gap is the cost of behavioral biases.

Section 1: Meet Your Internal Saboteurs

Your brain is running software that was never designed for the stock market. Here are five of the most destructive cognitive biases that investors face — and the all-too-familiar ways they show up in real portfolios.

1. Loss Aversion Bias: The Asymmetry of Pain

In their landmark 1979 paper Prospect Theory: An Analysis of Decision Under Risk, Kahneman and Tversky demonstrated something counterintuitive and profound: the psychological pain of losing $1,000 is roughly twice as powerful as the pleasure of gaining $1,000. We are not wired to evaluate outcomes symmetrically.

In practice, this means investors hold onto losing positions far longer than any rational framework would justify, waiting — hoping — for the stock to “come back.” The loss hasn’t been realized yet, so psychologically, it hasn’t fully happened. Selling feels like defeat. Meanwhile, the capital sits trapped in a deteriorating position while better opportunities are missed. Loss aversion doesn’t protect your wealth. It just delays and deepens the damage.

2. Overconfidence Bias: The Illusion of the Edge

Kahneman’s masterwork Thinking, Fast and Slow (2011) dedicates substantial exploration to what he calls the “illusion of skill” — our tendency to overestimate the accuracy of our own predictions and the quality of our own judgment. Studies have consistently shown that most individual investors believe they are above-average stock pickers. Mathematically, of course, most investors cannot be above average, some will be below.

Overconfidence manifests as excessive trading — trading a portfolio frantically based on the belief that you can time the market better than the collective intelligence of millions of other market participants. It also manifests as underdiversification: making concentrated bets because you’re sure about this one. Transaction costs, tax drag, and losses from being wrong compound quietly over time, eroding returns with surgical precision.

3. Confirmation Bias: The Echo Chamber1 in Your Head

The human mind is not a truth-seeking machine. It is a belief-confirming machine. Once we form an investment thesis — “this company is a buy” — we unconsciously filter all subsequent information through that lens. We read the bullish analyst report. We skip the bearish report. We join the Reddit investment thread full of believers and mute the skeptics.

Tversky and Kahneman described this phenomenon within their broader framework of cognitive heuristics: we anchor to an initial belief and then adjust insufficiently when new data arrives. In investing, confirmation bias means you’re rarely getting an accurate read of a situation — you’re getting a curated narrative that flatters what you already believe. By the time reality forces its way through, it’s often too late.

4. Herd Mentality: The Comfort of the Crowd

There is deep evolutionary logic to following the herd. If everyone around you is running, something dangerous is probably coming. But in financial markets, the crowd is often late — and sometimes catastrophically wrong.

Herd behavior is what drives asset bubbles and panic selling. It’s what caused retail investors to flood into tech stocks at the peak of the dot-com boom, cryptocurrency at its 2021 highs, and meme stocks at their frenzy peaks. It’s also what caused mass capitulation selling at the March 2020 COVID lows — right before one of the sharpest market recoveries in history. The crowd feels safe. The crowd feels validating. The crowd also, with remarkable reliability, buys high and sells low.

5. Regret Aversion: The Paralysis of “What If”

Perhaps the most insidious bias of all is one that doesn’t even require you to act. Regret aversion is the fear that if you make a decision — even the right one — and it goes wrong, you’ll feel worse than if you had done nothing and suffered the same loss passively.

This manifests as the investor who won’t sell a clearly deteriorating stock, not because they believe in the company, but because selling would mean admitting the original purchase was a mistake. It manifests as refusing to rebalance, refusing to cut losing positions, and refusing to pivot strategies — all to avoid owning a decision that could be wrong. Inaction feels safe. But in investing, inaction is always a choice, and it carries its own very real costs.

Section 2: The Real-World Cost — What This Is Actually Doing to Your Returns

These biases are not abstract philosophical curiosities. They have dollar signs attached to them.

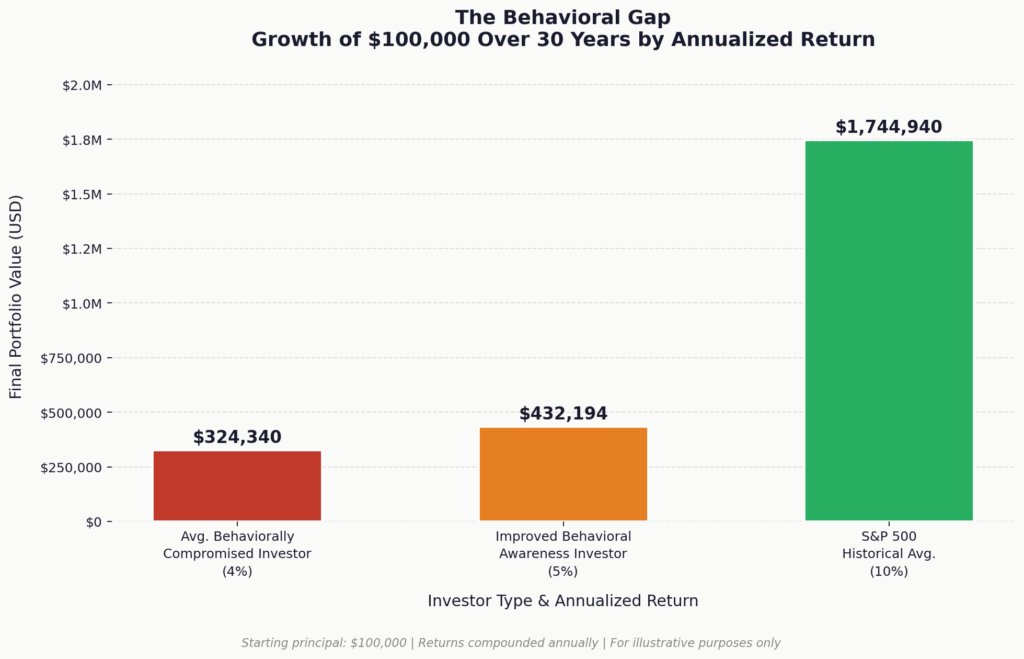

Consider the behavioral gap in concrete terms: if the market delivers 10% annually over a 30-year investment horizon, a $100,000 portfolio grows to approximately $1,744,940. If the average behaviorally-compromised investor captures only 4% of that same period — due to poor timing, excessive trading, and emotionally-driven decisions — that same $100,000 grows to only $324,430. The gap is over $1,400,000 not from picking the wrong stocks. This is drag from behavioral interference and cognitive biases alone.

Beyond the financial cost, consider the human cost. The investor caught in loss aversion lies awake checking pre-market prices. The overconfident trader rides a concentrated position downward, watching a year’s gains evaporate in weeks. The confirmation-biased investor, surrounded only by their own echo chamber, is blindsided by a thesis collapse they never saw coming. The herding investor sells in a panic and then watches the market recover without them.

This is not just about money. It is about the stress that strains relationships. The anxiety that occupies headspace. The sleepless nights that erode health and judgment. The compound effect of cognitive biases reaches far beyond your brokerage account.

Kahneman describes two systems of thinking in Thinking, Fast and Slow: System 1, which is fast, intuitive, and emotional; and System 2, which is slow, deliberate, and logical. Investing demands System 2 thinking. But under pressure — when the market is down 15%, when your neighbor just made a fortune on a speculative position, when the headlines are screaming — System 1 takes the wheel. And System 1 was never built for the stock market.

Section 3: What You Can Actually Do About It

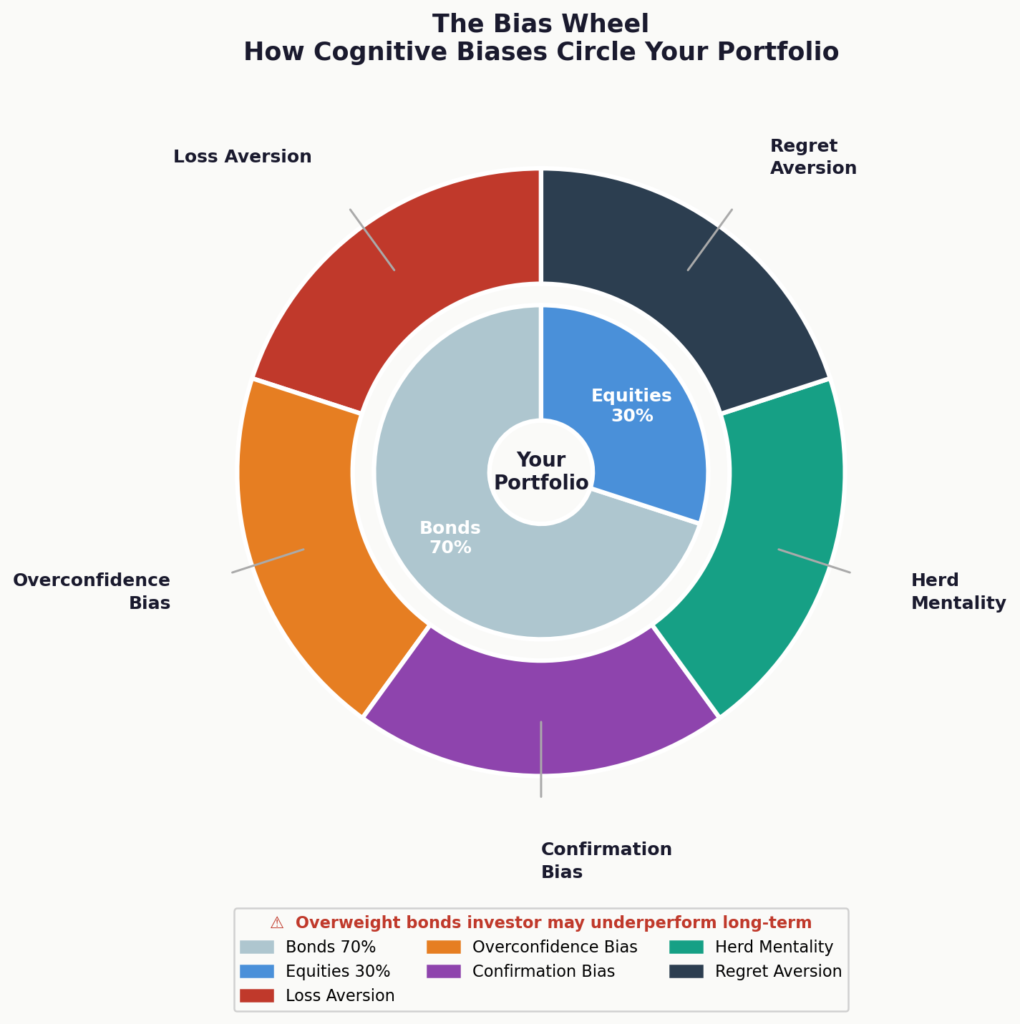

Awareness is not enough to eliminate cognitive bias — but it is the irreplaceable first step. You cannot course-correct what you cannot see. Begin by auditing your own recent decisions: Were you holding a loser too long? Were you reading only bullish commentary on a favorite position? Did you make a move because “everyone else was”? Simply naming the bias you’re operating under in the moment creates a critical pause between impulse and action. The bias wheel can be an effective tool to map how the five biases circle your own portfolio.

The next step is the construction of a process-driven decision framework — a set of rules and criteria you define in advance, when emotions are neutral, that govern how you will enter positions, size them, and exit them. A rules-based system doesn’t eliminate uncertainty, but it removes your emotional state from the equation. When the framework says sell, you sell. When it says hold, you hold. The rules — not your fear, not your hope — make the call.

Finally, consider the profound value of an objective external perspective. One of the most documented findings in behavioral research is that we are far better at identifying cognitive biases in other people than in ourselves. This is precisely why even elite investors — those who understand every bias intellectually — benefit from having a sounding board who is not invested in the outcome, not subject to the same emotional state, and trained to recognize the behavioral patterns that compromise decisions.

This is the domain of behavioral financial coaching: not just portfolio management, but the systematic identification and mitigation of the psychological forces that silently undermine even the most sophisticated investor’s results.

Conclusion

Your brain is your most powerful asset — but it also has its blind spots. The biases outlined above are not signs of weakness or lack of intelligence. They are features of human cognition, documented by the most rigorous behavioral scientists of our era. The investors who outperform over the long run are not those who are free of these biases — no one is. They are the ones who have built the self-awareness, the processes, and the support systems to keep those biases from making their portfolio decisions for them. Understanding your behavioral blind spots is not just useful in investing. It may be the single highest-return investment you ever make.

Ready to stop fighting your own mind? Learn how data-driven behavioral coaching can transform your investment approach — and finally close the gap between what the market offers and what you actually keep.

[Schedule a complimentary discovery call today →]

References: Kahneman, D. (2011). Thinking, Fast and Slow. Farrar, Straus and Giroux. | Kahneman, D. & Tversky, A. (1979). Prospect Theory: An Analysis of Decision Under Risk. Econometrica, 47(2), 263–291. | DALBAR, Inc. Quantitative Analysis of Investor Behavior (annual series).